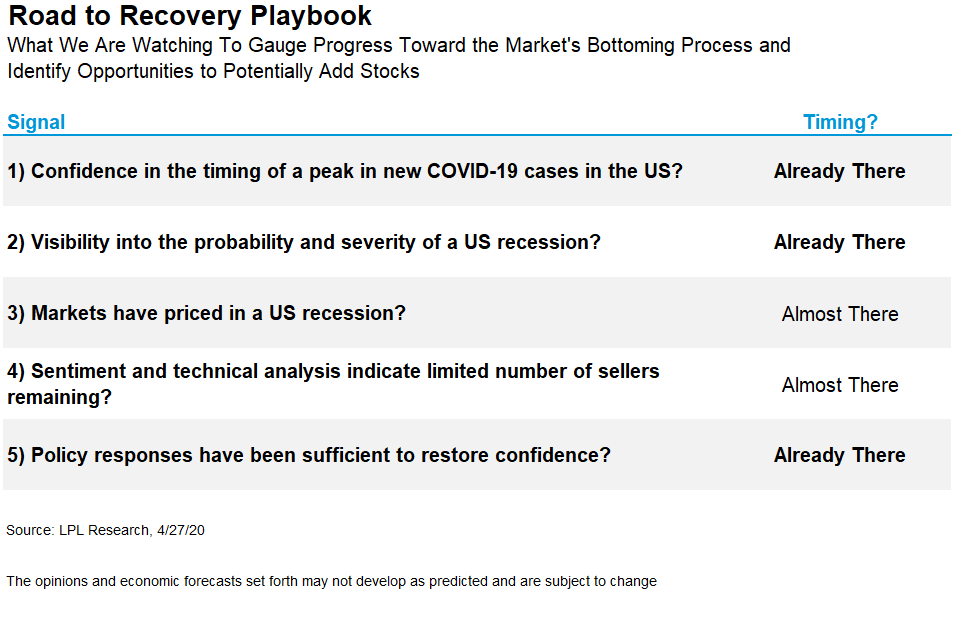

We continue to follow our Road to Recovery Playbook for help determining where the market is in its bottoming process and yesterday we upgraded Signal #1, confidence in timing of a peak in new COVID-19 cases, to “Already there.”

“Three of the five signals from our Road to Recovery Playbook are now in place,” said LPL Financial Equity Strategist Jeffrey Buchbinder. “With the S&P 500 Index more than 25% off its lows, stocks are no longer pricing in a recession and are no longer oversold from a technical analysis perspective, making the near-term risk-reward trade-off less favorable. We believe a more attractive entry point may emerge soon.”

Assessing the peak of the impact of COVID-19 on the US has probably been the most difficult signal in the Playbook to call with any degree of certainty, due to the unprecedented nature of this outbreak and the many data points available—new cases, hospitalizations, deaths, recoveries, testing rates, positive tests, etc. All of these factors have stabilized or improved in recent weeks. Even in New York, the epicenter of the US outbreak, most data points are at multi-week lows with new hospitalizations on course to trend to near zero by early May.

One of the most impactful factors influencing the number of new COVID-19 cases appears have been the availability and rate of testing performed. For this reason, we now may be at a point where even a slight rise in the number of positive test results is not necessarily bad news.

As shown in the LPL Chart of the Day, since the first week of April, the number of new COVID-19 cases in the US has remained fairly steady, even as the testing ramped up significantly in the last week.

Increased testing rates are beneficial because they provide a clearer picture of the scope and deadliness of the virus. The number of tests per positive result in the US has been falling in recent weeks but has not yet reached the World Health Organization (WHO) guideline of 10% positive results, indicating that there is still work to do to increase testing enough to capture the majority of people who have been infected.

Additional data published in recent COVID-19 antibody tests (albeit with small sample sizes) in San Francisco, Los Angeles, and New York all appear to suggest far more widespread asymptomatic or mild symptom prevalence of the virus in the general population. This would suggest that as testing increases, there may be an absolute increase the number of new cases but that it will not translate into more hospitalizations or deaths. Again, this wider prevalence is good news, as it implies that the overall hospitalization and case fatality rates are much lower than originally feared.

As many states across the US allow businesses to reopen, relax stay-at-home orders, and ease travel restrictions, LPL Research acknowledges that another wave of new cases is possible. Should another wave hit—of course we certainly hope it doesn’t—we expect the healthcare system may be in a better position to handle it.

Given the pre-outbreak economic strength, the apparent transitory nature of the threat, and massive stimulus, we expect a recession to be short in duration, but likely deep. Even with the S&P 500 up so much from the March lows, we continue to like the opportunity for long-term investors and maintain our overweight equities recommendation for suitable investors.

Next Step: Speak to a Financial Advisor

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

If your representative is located at a bank or credit union, please note that the bank/credit union is not registered as a broker-dealer or investment advisor. Registered representatives of LPL may also be employees of the bank/credit union.

These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of, the bank/credit union. Securities and insurance offered through LPL or its affiliates are:

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use | Tracking # 1-05003948