The November reading for the Consumer Price Index (CPI), the most well-known measure of inflation, was released Thursday, December 12, and while both the headline and “core” readings (excluding food and energy) came in slightly higher than the Bloomberg-surveyed economists’ consensus, core inflation remains tame at 1.6% over the trailing year. Inflation is likely to pick up as the economy improves and may run a little hotter than we’ve seen in recent years in 2021, but we believe the risks of a substantial inflation surprise over the next year is limited.

“Congress and the Fed provided massive stimulus this year and it seems like that should be inflationary,” said LPL Chief Market Strategist Ryan Detrick, “but it’s important to remember that the stimulus was there to fill a giant hole from lost wages and an economy running well below its potential.”

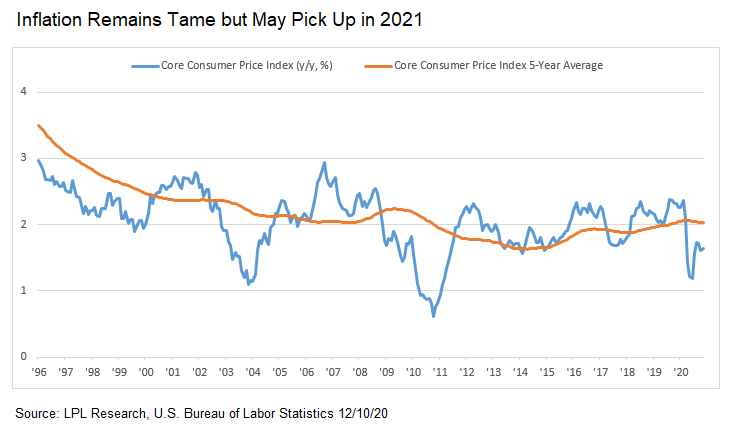

As shown in today’s LPL Chart of the Day, core inflation on a trailing-year basis still has some catching up to do, although the one-month reading is now largely consistent with pre-Covid levels. inflation over the last decade has remained subdued and largely steady.

INFLATION MAY RUN HOTTER

Core inflation has not hit 2.5% since 2008 and hasn’t hit 3% since 1996. Both levels may be reachable toward the middle of next year due to the short-lived inflation spike in June, July, and August 2020 as prices normalized, and may remain somewhat elevated as the economy recovers while the Federal Reserve likely keeps rates low. A falling dollar also tends to be inflationary, making foreign goods more expensive and COVID-19 could also create some supply chain disruptions, which may temporarily lift inflation.

FORCES THAT MAY HELP KEEP INFLATION IN CHECK

At the same time, there’s reason to believe inflation may have a ceiling in the 2.5 –3% range:

- The conditions that limited economic growth, and inflation with it, before COVID are still in play. Workforce growth is slowing, populations are aging, especially in developed economies, and productivity gains have been limited despite strength in some areas of the economy.

- Wage pressure is likely to be limited as long as there’s still slack in the labor market.

- The economy may continue to have spare capacity until it returns to long-term potential growth levels.

- Technological developments and increased use of green energy sources has steadily lowered the energy intensity of economic growth, decreasing the likelihood of energy supply shocks.

- Inflation historically bottoms early-to-mid expansion and only becomes a threat later in the business cycle.

We are likely to see trailing-year inflation numbers in the middle of next year that we haven’t seen in a while, but the monthly run rate will probably be less elevated. We do think we’ll see inflation run hotter than it has in recent years, but after years of central banks failing to push inflation towards 2%, we don’t yet see the kind of structural shift that could lead to inflation becoming a serious economic risk looking out over the next year.

Do you have our 2021 Market Outlook? Request it free!

Book a consultation or contact us today.

Book a consultation or contact us today.

Our 2021 Market Outlook is here! What does the stock market in 2021 have in store for us? 2021 will bring advances to further limit the impact of COVID-19, and the goal remains keeping the economy as open as possible until then. Continued progress in the response to COVID-19, including further stimulus, will be key to sustaining the recovery. As the pandemic subsides, restrictions are lifted, and consumers’ daily lives return to something close to normal, the pace of the recovery should pick up speed—probably in the middle of 2021.

Prepare to power forward in 2021 with the economic insights and market guidance in LPL Research Outlook 2021: Powering Forward.

Do you have a written financial plan to grow your net worth and protect your retirement? Set up a consult to get a financial plan and advice you can understand.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

If your representative is located at a bank or credit union, please note that the bank/credit union is not registered as a broker-dealer or investment advisor. Registered representatives of LPL may also be employees of the bank/credit union.

These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of, the bank/credit union. Securities and insurance offered through LPL or its affiliates are:

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use | Tracking # 1-05088725